A Will Is Not an Estate Plan

What high-net-worth families in Singapore need to understand about estate planning — and why the gap between having a document and having a structure can cost more than they realise.

Most people who’ve done the work have a will. Some have had it sitting in a drawer for years. A few have updated it since the last time life changed significantly. Almost none have asked whether the will is structurally sound enough to do what they actually need it to do.

That distinction — between having a document and having a structure — is the gap that costs families the most. Not in legal fees. In frozen assets, stalled distributions, family conflict, and wealth that was meant to last one more generation quietly dissolving in administrative friction.

A legally valid will is not the same as a structurally sound estate plan.

This is not a legal article. The author of this article is not a lawyer, and nothing here constitutes legal advice. What this is — is an architectural lens. One shaped by the observation that the families who suffer the most in estate transitions are rarely those who had no documents. They are the ones who had documents that were never designed to hold under the weight of real complexity.

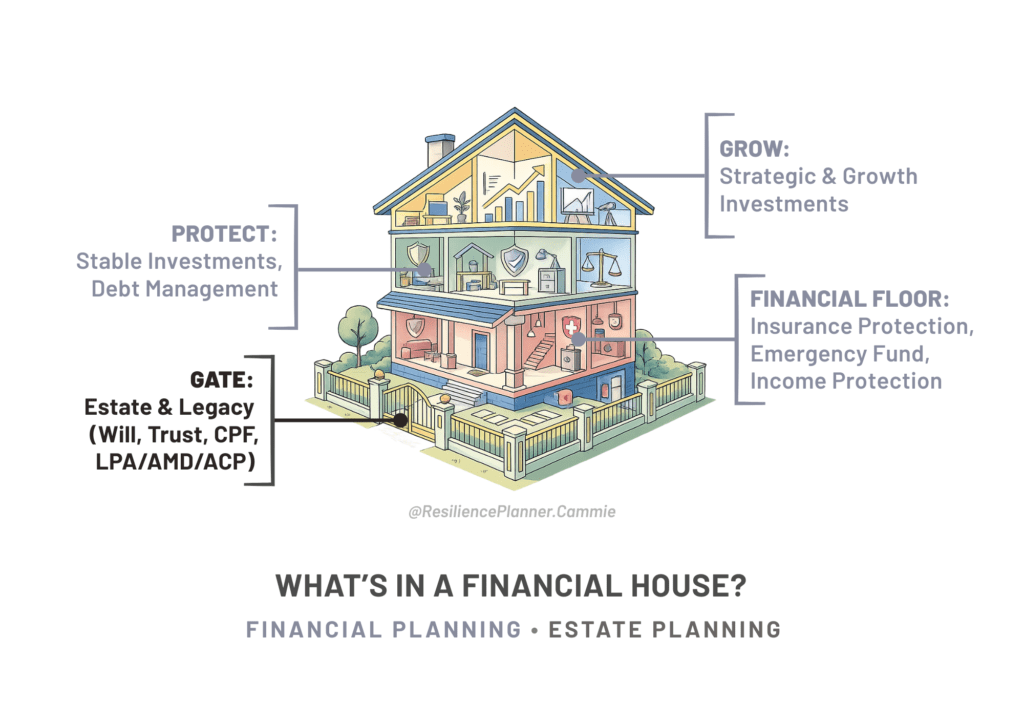

The Gate in the Financial House

In the Financial House framework, estate planning sits at the Gate — the structure that determines what passes through, to whom, under what conditions, and when. The Gate is the last element most people build, and the first one that matters when they are no longer around to explain their intentions.

The Gate is not just a will. It is the coordinated system of instruments that together determine how a financial life transitions: the will, trusts, CPF nominations, Lasting Power of Attorney (LPA), Advanced Medical Directive (AMD), and legacy planning that reflects not just asset distribution but values, continuity, and family governance.

When any part of that Gate is missing — or present but misaligned — the whole system can stall. And for high-net-worth (HNW) families carrying complexity across multiple asset classes, jurisdictions, and generations, a stalled estate is not a minor inconvenience. It is a years-long crisis that lands on the people least equipped to absorb it.

Why a Basic Will Falls Short for Complex Estates

A standard will does a specific job: it identifies executors, distributes assets outright, and in some cases names guardians for minor children. For straightforward estates, that job is sufficient. For high-net-worth families, it is a starting point — and often a fragile one.

Outright distribution of significant assets exposes beneficiaries to risks that the testator almost certainly did not intend. Assets that pass directly into a beneficiary’s name become matrimonial in character once they are commingled or used for family purposes — which means divorce proceedings can reach them. Creditor claims follow the same logic. A large inheritance received by a beneficiary who lacks financial maturity is not a gift; it is a liability waiting to be expressed.

The will also cannot do what is needed across jurisdictions. Singapore law governs what Singapore law governs. Overseas properties, foreign bank accounts, offshore structures, and assets held in civil law countries are subject to their own rules — including forced heirship regimes that override testamentary intent and probate resealing requirements that add time, cost, and complexity to every international distribution.

The estate plan that works for one jurisdiction may actively conflict with the rules of another.

For globally mobile families — the Singapore permanent resident with a property in Australia, the dual citizen holding investments in the UK, the expat whose financial life spans three countries — this is not a theoretical concern. It is the most predictable source of estate administration failure, and it is almost entirely avoidable with the right architecture in place before it is needed.

Testamentary Trusts: Building Control Into the Gate

One of the most powerful tools available to Singapore families with complex or multi-generational wealth is the testamentary trust — a trust created by the will itself, activated upon death rather than during lifetime.

A testamentary trust does not distribute assets immediately or unconditionally. It can stagger distribution by age or milestone, allowing capital to remain managed and protected while beneficiaries mature. It can ring-fence inherited assets from matrimonial exposure. It can provide discretionary income to dependants whose needs are not uniform or predictable. It can preserve capital for long-term growth while a professional trustee provides structured oversight.

For business-owning families, this matters even more. Business interests that form a substantial portion of the estate require succession planning that runs alongside — not inside — the personal will. Without structured business succession, the death of a founder or majority shareholder triggers a cascade that a simple will has no capacity to manage: shareholder disputes, liquidity crises, forced asset sales, leadership vacuums, and family relationships that fracture under the weight of decisions that should have been made years earlier.

Key instruments to consider in a structurally sound estate plan:

- Will with testamentary trust provisions — coordinates outright and managed distribution across beneficiary needs and risk profiles.

- CPF nomination — CPF assets do not pass through the will. A separate, current nomination is essential and must be reviewed after every major life change.

- Lasting Power of Attorney (LPA) — the instrument most commonly deferred and most acutely needed. An LPA designates a donee to manage financial and personal welfare decisions if the creator loses mental capacity. It must be registered before capacity is lost — after which it cannot be made.

- Trust overlays for business interests — shares held in a trust structure allow continuity of control and can separate economic interest from governance in ways a will cannot.

- Multiple wills for multiple jurisdictions — for globally mobile families, separate jurisdiction-specific wills (carefully coordinated to avoid unintended revocation) are often more efficient than a single document attempting to govern everything.

- Digital asset instructions — cryptocurrency, online investment accounts, intellectual property, and digital royalties require documented access protocols. Without them, executors may face assets they legally own but cannot access.

Liquidity: The Structural Gap Most Plans Miss

Estate plans frequently address distribution but neglect liquidity — the availability of accessible funds to meet immediate obligations at the point of death and during the administration period. For estates comprising primarily real property, private company shares, or illiquid investments, this gap can be severe.

Debt obligations do not pause for estate administration. Foreign tax liabilities — estate or inheritance taxes in jurisdictions where assets are held — must be settled. Dependants need income continuity. Properties require maintenance and upkeep during a protracted distribution process.

Insurance nomination structures play a central role in liquidity planning. Proceeds from a nominated life insurance policy are available immediately, outside the estate, without waiting for probate. For estates that are asset-rich but cash-poor, this single instrument can be the difference between a dignified transition and a forced asset sale.

The question is not just what you are leaving behind. It is whether there is enough liquidity to hold everything together while it is being transferred.

The Professional Executor Question

For complex estates, the question of who administers the will is as important as what the will says. Appointing a family member as executor is the default — and for straightforward estates, it works. For HNW families, it introduces risks that are easily underestimated.

Executors carry fiduciary duties. They manage the estate’s affairs across what can be a multi-year administration process, navigate relationships with multiple beneficiaries, and make decisions that are simultaneously financial, legal, and relational. When the executor is also a beneficiary — or a sibling of beneficiaries — conflict of interest is not a remote possibility. It is structurally embedded in the appointment.

Professional executors — lawyers, licensed trust companies — bring neutrality, continuity, and institutional knowledge. They are not a replacement for family involvement in the legacy; they are the structural support that allows that involvement to remain relational rather than administrative.

Read more: How to choose an Executor for your Will?

Philanthropy and Legacy: Architecture for What Endures

Among established HNW families, there is a growing recognition that an estate plan is not only about what is distributed — it is about what is carried forward. Family values. A standard of stewardship. A relationship with wealth that the next generation inherits alongside the assets themselves.

Structured philanthropic planning — charitable trusts, donor-advised funds, family foundations, conditional legacy gifts — integrates giving into the estate architecture rather than treating it as an afterthought. When designed well, philanthropy reinforces family identity across generations. It creates structured decision-making around shared values. It becomes, in that sense, cultural stewardship rather than merely financial transfer.

Research consistently shows that family wealth dissipates by the second or third generation — not primarily due to legal inadequacy, but due to governance failure. The families that maintain wealth across generations are those who built the governance frameworks early: family constitutions, structured councils, independent trustees, clear protocols for wealth decision-making that do not depend on any single individual remaining at the centre.

Read more: Starting Your Giving Journey with Your Own Charitable Fund

What This Means Through the TRP Lens

The Financial House framework positions estate planning at the Gate — structurally, the last layer to be built, and the one that seals everything that came before it. But the Gate is not the end of the conversation. It is the test of whether everything else was built properly.

A financially resilient life is one where the Grow, Protect, and Preserve layers are coordinated — and where the Gate reflects the actual complexity of what has been built. Not a document written once and filed away. A living structure, reviewed whenever life changes significantly: a marriage, a divorce, a birth, a business sale, a property acquisition across a new jurisdiction, a health event that changes capacity planning.

I came to understand this not from a textbook but from the point of having been uninsurable — of having seen, firsthand, what it costs when the system that was meant to protect you was not designed for your circumstances. I built my own financial floor first. Then I built the frameworks. The Gate was the last thing I designed, and the most precise.

Most of the families I work with have done a great deal right. They have accumulated. They have protected. They have grown. What they often have not done is closed the Gate properly — or tested whether what they have in place will actually hold under the weight of real complexity.

Intention without executability is not a plan. It is a wish.

A Starting Point

If any part of this has prompted a question — about whether a current will reflects current complexity, whether CPF nominations are current, whether an LPA is in place, whether a globally held estate has been structured for the jurisdictions it actually spans — that question is worth pursuing.

The Wealth Seasons quiz is a useful first step for understanding where a financial life currently sits, structurally. From there, the conversation about the Gate becomes more specific, more grounded, and more useful.

The building is already up. The question is whether the Gate is equal to it.

You Don’t Have to Figure This Out Alone

If this raised questions about your finances, a Clarity Call gives you space to pause and see your situation more clearly.

In this conversation, we focus on:

• where your financial structure stands today

• what deserves attention now — and what can wait

• the next steady step forward, without pressure

A calm, no-pressure conversation to help you move forward with clarity.

Disclaimer: This content has not been reviewed by the Monetary Authority of Singapore and is not affiliated with or endorsed by any Singapore government agency. References to “Singapore” refer only to the geographical area served. The information is for general knowledge and educational purposes only, is accurate at the time of writing, and may be subject to change. It should not be considered financial or legal advice. Please consult a licensed financial advisory representative or legal advisor for personalised recommendations. E&OE.

About the author: Cammie currently holds a financial advisory license for distribution of insurance and collective investment scheme products, and has an Estate Succession Practitioner certification. Trained as an Architect and being a brain tumour survivor, she identifies herself as The Resilience Planner in Personal Finance. Her approach to financial advisory is consultative – she encourages her clients to be participative and ask questions. She believes that because Personal Finance is personal, she works with clients to create tailored solutions that suit each individual’s unique needs and life goals.